4 Things to Do on Your 65th Birthday to Save Money

Turning 65 is a huge milestone for many people. Not only can you qualify for Medicare, but you also may be eligible for lots of senior discounts!

You also have a lot of decisions to make. For example, the full retirement age to receive Social Security benefits used to be 65, but that’s changed to 66 ½ for people turning 65 in 2019. You must decide if you want to retire or continue working to receive full benefits. If you don’t make a decision, you could be missing out on a lot of money. Use this list of four things to do on your 65th birthday to save money now.

Turning 65 Checklist

1. Enroll in a Medicare Plan.

You can potentially save thousands of dollars if you enroll in the right kind of Medicare plan on time.

When You Can Enroll in Medicare

Many people are eligible to enroll in Medicare during their Initial Enrollment Period (IEP), which is the three months before your 65th birthday, your birthday month, and the three months after your 65th birthday. Note: That IEP is only for people who qualify for Medicare because of their age. If you qualify for Medicare because you’ve been diagnosed with ALS, ESRD or you’ve received SSDI for at least 25 months, your IEP will begin when you become eligible.

If you don’t enroll during your IEP, you may face up to 10 percent of your premium costs in late enrollment penalties. However, you may be able to delay Medicare Part B enrollment if you receive coverage through your or your spouse’s employer.

If you lose employer coverage you may be eligible for a Special Enrollment Period (SEP), which will allow you to enroll in a new plan.

That covers when you may be eligible to enroll in Medicare insurance, but you may not know what kind of policy you need. Original Medicare helps pay for many hospital and outpatient services, but it doesn’t cover everything. Many Medicare enrollees choose to add private insurance coverage to Original Medicare in order to cover the services they need.

Should I Choose Medicare Advantage or Medigap?

You may have the option of choosing a Medicare Advantage or a Medigap (Medicare Supplement) plan. Both options can help pay for items that Original Medicare does not. You cannot have both a Medicare Advantage (MA) plan and a Medicare Supplement plan, so it’s important to understand the distinction between the two:

Medicare Advantage can add additional benefits such as prescription drugs, hearing, dental, vision, and even fitness classes! MA plans help pay for healthcare services.

Medicare Supplement plans cover financial items such as coinsurance and deductibles.

It’s ultimately up to you to decide which type of plan you need, and it might be confusing. If you want help deciding which plan is right for you, a licensed agent with Medicare Plan Finder can help. Your agent will discuss your needs and can help you find a plan that fits your budget and lifestyle. Call 844-431-1832 or contact us here to set up a no-cost, no-obligation appointment.

Contact Us | Medicare Plan Finder

2. Consider Purchasing Long-Term Care, Life, and Final Expense Insurance.

Even though it may seem uncomfortable, considering long-term care, life, and final expense insurance may be one of the most important things to do on your 65th birthday. Planning ahead can help you and your loved ones save a lot of money in the long-run.

Long-Term Care Insurance

Many people will need long-term care at some point in their lives, and it can be expensive. You may be able to save money by purchasing an insurance plan to help pay for your needs.

Original Medicare doesn’t cover long-term care unless it follows a hospital stay or it’s medically necessary. While you can use a Medicare Supplement plan to help pay for copays, some Medicare Advantage plans may offer a long-term care benefit.

Life Insurance

A life insurance policy can help your loved ones financially after you pass away. You can save money in monthly premiums the earlier you enroll depending on your type of policy.

Final Expense Insurance

While long-term care insurance can help cover medical expenses and life insurance can help your loved ones after you die, final expense insurance helps cover funeral and burial costs. A final expense policy can help your loved ones carry out your last wishes after you pass away.

Final Expenses and Arrangements Guide

3. Sort out Your Legal Affairs.

If you haven’t already, getting your legal affairs in order is a crucial thing to do on your 65th birthday. Even though the average life expectancy in the United States is over 79 years old in 2019, accidents and chronic illnesses can happen at any moment, unfortunately. Now is the time to get your wishes sorted out regarding healthcare and your estate.

Think about what choices you have and how they will affect your and your loved ones’ future. Then organize your personal and medical files.

Power of Attorney

Find an elder law attorney and meet about drafting a legal will and designating your power of attorney, which is a document that allows a person of your choosing to make legal decisions on your behalf. There are different types of power of attorney that take effect in different circumstances. Your lawyer will help you assign the right kind of power of attorney to the person you choose.

You may also want to discuss a living will (medical directive), which is a document that ensures your medical wishes are carried out, with your lawyer.

Choosing Power of Attorney | Medicare Plan Finder

4. Take Advantage of Senior Discounts!

Many companies offer discounts to people just for turning 65. You can receive discounts on items ranging from restaurant meals to plane tickets. According to SeniorLiving.org, Southwest Airlines offers reduced fares for anyone 65 and older.

You can also get discounts on prescription drugs from many pharmacies! Download this prescription drug discount card to receive huge savings on the prescriptions you use every day.

Free Prescription Discount Card

You’re Turning 65 and Medicare Plan Finder Can Help.

If you’re turning 65, Medicare Plan Finder can help you get the insurance coverage you need. Our agents can help you determine what plan will help you save the most money. Want to learn more? Call 844-431-1832or contact us here to arrange an appointment today.

Contact Us | Medicare Plan Finder

7 Common Medicare Mistakes to Avoid

Choosing the right Medicare plan for you can seem daunting. You may be confused about what plan to buy or frustrated that you can’t find the information you need to make a sound choice.

You don’t want to potentially be stuck paying huge penalties or have a plan that doesn’t work for you. However, if you have the right knowledge, you can steer clear of the hassle that comes with these seven common Medicare mistakes to avoid.

1. Waiting Until It’s too Late to Sign up for Medicare

Medicare Late Enrollment Penalty | Medicare Plan Finder

If “timing is everything,” that goes double for Medicare enrollment. One of the most common Medicare mistakes to avoid is putting off enrollment until it’s too late. Many people know that you can enroll in Medicare when you’re 65, but what they might not know is that you can actually start the process when you’re 64. The three months before your 65th birthday, the three months after your birthday, and your birthday month is what’s called the Initial Enrollment Period (IEP).

You can avoid costly penalties if you sign up during your IEP. If you sign up to late your Medicare Part B premium may go up 10 percent for each year that you could have been covered but didn’t enroll.

The IEP doesn’t apply to everyone. For example, people with certain chronic conditions or people who’ve received SSDI benefits for at least 25 months may be eligible for a lifelong Special Enrollment Period (SEP). If you qualify, your lifelong SEP will allow you to make changes to your coverage once per quarter for the first three quarters of the year.

People who go through certain life changes such as losing coverage upon retirement or losing a spouse’s coverage can sign up for Medicare during a temporary SEP, which allows you to enroll late without paying a penalty. However, a circumstantial SEP is only for eight months after you stop receiving employer coverage, so it’s crucial that you enroll during that time frame.

3. Thinking You’re Covered Just Because Your Spouse Has Coverage

Employer insurance plans usually come with an option that covers you and your spouse. Medicare does not work that way. You and your spouse each need an individual plan.

This is actually a good thing. When you were younger, it probably made more sense to not deal with multiple insurance carriers. However, as you age, you become more susceptible to certain illnesses, and you may have different needs than your spouse. You may need more or less covered services.

For example, you might only need to visit your doctor every once in a while for wellness exams or the occasional sickness. However, your spouse may need to look into enrolling in a special type of plan called a Chronic Special Needs Plan (C-SNP) because of a chronic illness.

4. Not Using the AEP to Make Changes or Enroll in New Plans

If you don’t take advantage of the Annual Enrollment Period (AEP), which is October 15 – December 7, you could be stuck with a plan that doesn’t fit your needs for another year.

For example, if you only have Original Medicare and you want to capitalize on the supplemental benefits Medicare Advantage plans can offer, AEP is your window of opportunity.

5. Assuming Medicare Is Unaffordable

Some people may put off enrolling in Medicare because they think they can’t afford it.

While Medicare isn’t free, many people can get premium-free Medicare Part A. You will not owe a Part A premium if you or your spouse has worked and paid Medicare taxes for more than 40 quarters.

Even though you may have to pay premiums for Part B and other Medicare coverage, there is help available. If you have a limited income, you may be able to find assistance through certain Medicare programs such as Medicare Savings Programs, Low Income Subsidy Extra Help, and state Medicaid programs.

Medicare Savings Programs (MSPs): These programs can help pay the Part B monthly premium and help out with coinsurance fees, depending on the program. (There are currently three types of MSPs).

Low Income Subsidy (LIS) Extra Help: This federal program can help pay for the costs associated with Medicare Part D prescription drug coverage.

State Medicaid Programs: This program is funded by both federal and state resources. Medicaid provides medical assistance for people with low incomes and few assets. All Medicaid programs provide certain coverages such as prescription drugs.

Free Prescription Discount Card

People who qualify for MSPs or LIS may also qualify for Medicaid. If you’re eligible for both Medicare and Medicaid, you can enroll in what’s called a Dual Special Needs Plan (DSNP). A DSNP may help pay for most or all of your healthcare costs.

6. Thinking Medicare Covers Everything

Common Medicare Mistakes to Avoid | Medicare Plan Finder

Original Medicare (Part A and Part B) is a great resource for helping out with healthcare costs, but it doesn’t cover everything. Medicare Part A covers inpatient services at hospitals. Medicare Part B covers outpatient services such as doctor’s appointments. Even with those services, you’ll still owe your monthly premium and coinsurance if you see your doctor. For example, the fee for Part B services is usually 20 percent of Medicare-approved costs.

Original Medicare doesn’t cover many services people need such as vision, hearing, and dental care. The Centers for Medicare and Medicaid (CMS) allows private insurance plans called Medicare Advantage (MA) plans to provide those services.

Not every plan in every location offers those extra services, so it’s a good idea to talk to someone who can help you find the plans available in your area if those services are important to you. A licensed agent with Medicare Plan Finder can help you determine what type of Medicare plan is right for you.

For some people, Medicare Advantage plans may not make sense, but they still need more coverage than Original Medicare provides. Some people may only need help with financial items such as coinsurance fees. Those people might benefit most from a Medicare Supplement (Medigap) plan. While MA plans help cover healthcare services, Medigap plans only cover costs.

Find Medicare Plans | Medicare Plan Finder

7. Not Understanding What You Have to Pay out of Pocket

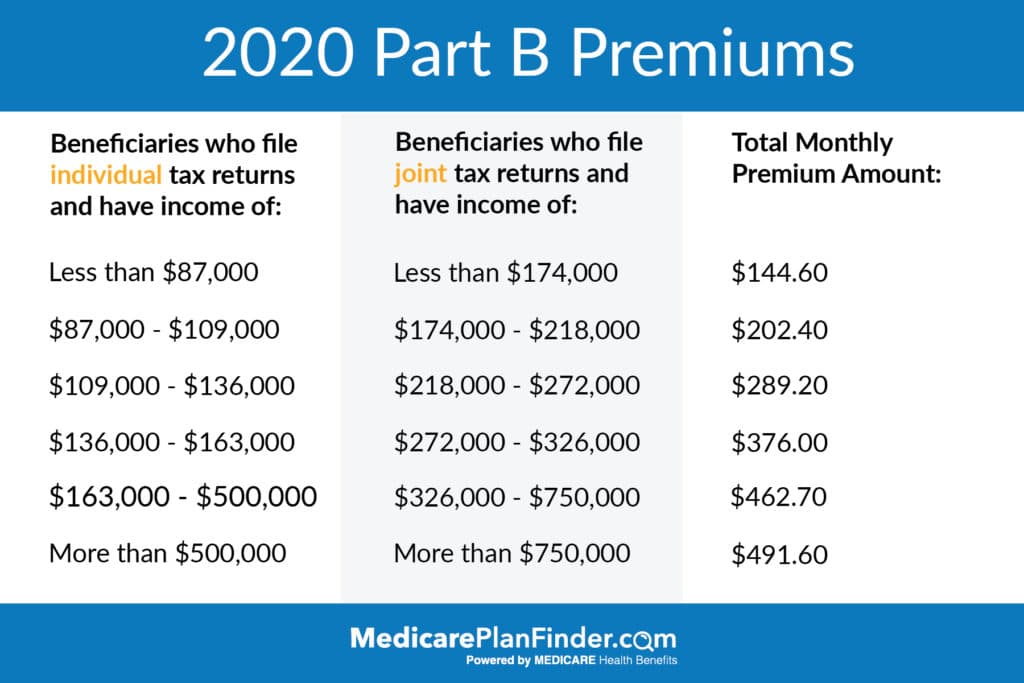

Even if you enroll in a Medicare Advantage or Medigap plan, you may still owe monthly premiums. That means that even though your Medicare Advantage plan may have a $0 premium, you may also have to pay the Part B premium, which is $144.60 in 2020 (unless you have high income).

2020 Medicare Part B Premiums

You may also have to pay a deductible before your coverage starts. The Part B deductible in 2020 is $198. Your MA or Part D plan may also require you to pay a deductible.

You may also have to pay copays or coinsurance. You may owe a copay, which is a fixed amount you pay for services such as doctor’s appointments with many MA plans. Coinsurance is a percentage of covered services. Original Medicare pays about 80 percent of approved costs and you are responsible for the other 20 percent. Your cost sharing for covered services may be different if you’re enrolled in a MA or Medicare Supplement plan.

Let Us Help You Avoid Common Medicare Mistakes

Medicare can be confusing. You might not know what coverage you need or what type of plan fits your budget and lifestyle. A licensed agent with Medicare Plan Finder can show you what’s available in your area and help you choose the best plan for you. Your agent is familiar with the common Medicare mistakes to avoid and help you take the right steps. To schedule an appointment, call 844-431-1832or contact us here today.

Contact Us | Medicare Plan Finder

Why Medicare Advantage Plans Are Bad

Someone may have told you a million reasons why Medicare Advantage plans are bad. The truth is they’re just misunderstood. More than 34 percent of Medicare beneficiaries are enrolled in Medicare Advantage (MA) plans, so they can’t be all bad.

What Is Wrong With Medicare Advantage Plans?

Medicare Advantage plans have pros and cons like any other type of health insurance plan. They may not make sense for some people, but they can be extremely beneficial for others, and here’s why.

They Can Be Expensive

Why Medicare Advantage Plans Are Bad | Medicare Plan Finder

Medicare Advantage plans all come with monthly premiums. Some of them have $0-premiums, but the average monthly premium in 2019 is $28. Some people may think, “free,” when they hear “$0 premium,” but that’s not necessarily the case. Even if you enroll in a MA plan, you may still be responsible for paying your Medicare Part B premium and other costs, like copayments.

Along with monthly premiums, MA plans can come with high out-of-pocket maximums. An out-of-pocket limit is designed to protect you. Once you reach your limit, the insurance company pays for your covered services. However, some plans’ out-of-pocket limits can be as high as $6700.

The out-of-pocket limit resets at the beginning of the year, but you could end up paying $13,400 if you have two major procedures within a few months.

For example, if you have hip replacement surgery in November, you might reach the $6700 limit just from that. Then,after your out-of-pocket maximum resets in January, you need knee replacement surgery. You would owe another $6700, just a few months later. You would then be covered for the rest of the year, but that total of $13,400 within a few months can certainly hurt.

Medicare Advantage Plans Have Smaller Networks

Most MA plans have provider networks you have to stay within. You can go out-of-network to find a doctor, but you may have to pay significantly more than if you stayed in your network.

You may even go to your favorite doctor and get turned away because your doctor isn’t in your plan’s coverage network.

Many people don’t realize that MA plans have networks when they enroll, and that may be why Medicare Advantage plans are bad according to some people.

Specific Coverage Areas

Most MA plans have coverage specific to one location. That’s great if you’re close to home and you need medical treatment, but that means your plan may not cover a doctor’s appointment if you get sick when you’re out of town. Original Medicare is a federal program, so it is likely that you’ll be able to find a doctor when you’re on vacation in another part of the country.

Your Plan Could Change Every Year

Many Medicare Advantage plans change their benefits every year. Sometimes they add or remove providers, covered services, and/or prescription drugs on the plan’s formulary.

Plans can also change how much you pay in monthly premiums, copays, and/or deductibles.

That means you’ll have to change plans if your current plan drops vision coverage, and you signed up for your plan specifically because you wanted the annual eye exam benefit. The problem is that you can only change plans during certain parts of the year.

Most people have to wait until the Annual Enrollment Period (AEP), which is from October 15 – December 7 to enroll in new plans or make changes to existing ones. Exceptions to that rule include people who are about to turn 65, or who just had their 65th birthday.

The Initial Enrollment Period (IEP) for people aging into the program is the three months before you turn 65, and the three months after. During that seven-month period you can choose a new Medicare health insurance plan. If you are eligible due to ALS or ESRD, your IEP is the week after your diagnosis. If you are eligible due to receiving SSDI for at least 25 months, your IEP is your 25th month of benefits.

You may qualify for a Special Enrollment Period (SEP) if you meet certain conditions. Your SEP may be lifelong or temporary, but it will allow you to make changes to your plan outside of the other enrollment periods.

Some Plans Require Doctor Referrals

Many Medicare Advantage plans are HMOs, which require you to select a primary care provider (PCP). In most cases, your PCP will need to give you a referral before you can see a specialist.

To illustrate what this looks like, let’s take the example of a man* who has a MA HMO. The man notices a mole that’s changed in size and shape. He knows he needs to see a dermatologist because he’s had skin cancer before, and the new mole likes like his previous carcinoma.

The man can’t just go to a dermatologist, however. He needs to first make an appointment with his PCP, and the PCP can then refer him to a dermatologist. The man will owe a copay to see his PCP, and then he’ll need to pay the dermatologist a copay, too. Specialist copays are usually higher than PCP copays. You may pay $10 for a PCP visit, but $40 for a specialist.

On the flip side, because the man went to his primary physician first, he got a really good recommendation and was able to see one of the best dermatologists in his town on short notice. That doctor referral requirement may have brought more help than harm.**

*This example is not real and only represents a possible circumstance.

**Not all doctors will be able to see you on short notice, regardless of your plan.

Benefits of Medicare Advantage Plans

The reasons why MA plans are good may outnumber why Medicare Advantage plans are bad. The truth is everyone has different healthcare and financial needs. MA plans make sense for people who want coverage for a variety of health services.

Medicare Advantage Plans May Actually Cost Less

Even though you may still owe the Part B monthly premium, you could end up paying less overall if you have Medicare Advantage.

Your cost-sharing may also be less with a MA plan. If you only have Original Medicare, you will owe 20 percent of covered services, and Original Medicare will pay 80 percent of approved costs.

To illustrate what this looks like, let’s say you see your doctor because you have the flu. Your doctor charges Medicare $100. Medicare approves the charge and you owe $20.

Many MA plans have copays of $10 or less for doctor’s appointments. That $10 savings for one doctor’s visit may not seem like much, but it adds up over time.

Plans Can Be a “One-Stop-Shop” for Covered Services

Many Medicare Advantage plans are designed to provide the beneficiary with comprehensive healthcare coverage. MA plans can offer coverage for services Original Medicare does not, including vision, hearing, dental, and fitness classes.

Many MA plans even include prescription drug coverage, which Original Medicare does not.

That also means that you may have access to doctors with a variety of specialties, provided they’re in-network. All of your providers can coordinate with each other to provide a complete health plan to keep you in optimal health.

Fitness Class | Medicare Plan Finder

Find out Why Medicare Advantage Plans Are Bad (or Good) for You

A Medicare Advantage plan may be a good fit if you need coverage for a variety of services and you want to have a whole care team creating your treatment plan. A licensed agent with Medicare Plan Finder can help you determine if a MA plan is right for your budget and lifestyle needs. To get started, call us at 844-431-1832 or contact us here today.

As you age, it can become difficult to perform everyday tasks such as bathing or getting dressed, and you may need assistance to do those things.

Long term care may consist of skilled nursing services or physical therapy immediately following an illness or injury, or it may consist of someone coming to your house to help you with day-to-day tasks.

Does Medicare Cover Long Term Care?

Medicare Long Term Care Coverage | Medicare Plan Finder

Original Medicare does not cover long term care unless it follows a hospital stay or is for necessary medical treatment.

However, you can use certain Medicare Advantage (Part C) or Medigap (Medicare Supplement) insurance plans to help pay for non-medically necessary long term care. Here’s what Original Medicare will cover:

Medicare Skilled Nursing Coverage

Medicare Part A will cover short stays (100 days or less) in skilled nursing facilities if you meet these qualifications:

You’ve been admitted to the hospital for at least three days

A Medicare-certified skilled nursing facility admits you within 30 days of the initial hospital stay

Your treatment plan involves skilled care such as physical therapy or skilled nursing services.

Medicare will cover 100 percent of the costs for the first 20 days. In 2019, your copay for days 21-100 is $170.50.

For Medical Treatment

In order for Medicare to cover long term care for medical treatment, your doctor must first deem it medically necessary. Medicare Part B will cover the following services:

Intermittent and part-time skilled nursing care

Physical therapy

Occupational Therapy

Speech pathology

Your durable medical equipment (DME) can be covered if your doctor prescribes it and it will be used for at least three years. Medicare Part B also covers mental health services to help manage the psychological and cultural issues that come with having an illness.

There is no limit on how long you can receive the above services if your doctor reorders them every 60 days.

Chronic Special Needs Plans (C-SNP) will cover long term care services for people with chronic illnesses. The covered services for conditions such as Parkinson’s and ALS are to help prevent and slow the progression of the symptoms.

Original Medicare will NOT cover prescription drugs for chronic illnesses, however. Prescription coverage falls under Medicare Part D and certain Part C plans.

Part D Checklist | Medicare Plan Finder

Medicare Hospice Coverage

If you have a terminal illness with no chance of improvement, are expected to live less than six months, and are looking for peace instead of a cure, Medicare will cover hospice care.

In order for Medicare to cover drugs to control the symptoms and to relieve pain, you must be receiving care from a Medicare-approved hospice provider.

You can receive hospice care at your home, in a nursing home, or in a hospice care facility. When you enter hospice care, you will have an entire team of people focused on your overall comfort and well-being including your spiritual and emotional needs, not just your physical needs.

Long Term Care Coverage With Medicare Supplement Vs. Medicare Advantage

Private insurance companies offer plans that can go beyond what Medicare Parts A and B will cover. For non-medically necessary long term care, you won’t be able to use Original Medicare, and, for the most part, you won’t be able to use Medicare Supplements, either. If you want long term care coverage, a Medicare Advantage plan may be your best option.

Long Term Care Medicare Supplement

Medicare Supplements (Medigap) plans are designed to fill in the financial gaps Original Medicare creates. For example, you are financially responsible for that $170.50 copay. You can use a Medicare Supplement to help make those payments easier.

Medicare Advantage

Medicare Advantage (MA) plans are insurance plans that can cover medical services Original Medicare does not. While Medigap plans are strictly for help paying for out-of-pocket costs, MA plans are for additional medical coverage. Certain Part C plans can include coverage for DME and non-medical long term care, so it’s critical you know what your options are.

Note: You cannot have both a Medicare Supplement and a Medicare Advantage plan, so having someone help you sift through the thousands of plans out there and find the right one for you is extremely important to your overall health and well-being.

Medicare Advantage | Medicare Plan Finder

Why It’s Important to Have a Plan

Long term care can easily cost hundreds or thousands of dollars a month, and those costs will only increase. By 2050 the baby boomer population in the US will be 80 million, and that means more competition for home health care and therefore steeper prices. Having a health insurance plan to help with those costs might not only help you stay in good health, but also give you peace of mind.

Get Medicare Long Term Care Coverage Today

Are you looking for Medicare long term care coverage? One of our licensed agents can answer your questions and help you find the right plan for you. Fill out this form or call us at 844-431-1832 for a no-obligation appointment today.

Find Medicare Plans | Medicare Plan Finder

.

10 Great Apps for People With Dementia and Alzheimer’s

Dementia and Alzheimer’s are extremely debilitating disorders that severely hinder a person’s person’s quality of life. Dementia is an umbrella term for several disorders that can cause memory loss and other symptoms. One of the most common subsets of dementia is Alzheimer’s, which is a degenerative physical deterioration of the brain.

According to the Alzheimer’s Association, 33 percent of seniors die with Alzheimer’s disease or another type of dementia, and the tech world has taken note. Developers have created smartphone apps to help make your life a little easier. These 10 apps for people with dementia cannot cure the condition. They can, however, help slow memory loss and help you regain confidence.

1. Mindmate

Mindmate is a cognitive health maintenance app for people with dementia. It’s based on “world-leading science,” according to the developers.

The app features interactive games that are designed to stimulate the problem-solving, memory and attention centers of the brain.

Along with fun games, the app includes exercise programs, nutrition tips, and recipes. You can set goals and track your progress on the app, too, which makes Mindmate a pretty comprehensive brain health app.

2. My Reef 3D

My Reef 3D is great for people in the advanced stages of dementia. The app is a game that allows you to interact with 14 different types of fish. You can stock the aquarium and even tap on the glass to see how the fish react! Much like a real aquarium, you can sit back and watch the fish.

Many dementia sufferers won’t be able to pay attention to TV programs, but this app provides just enough stimuli to keep the user entertained.

3. Lumosity

Apps for People With Dementia | Medicare Plan Finder

Lumosity is a fantastic app for anyone with dementia. It’s a brain training program that uses daily games to test your critical thinking, memory, and problem-solving skills. The app analyzes your strengths and weaknesses and provides “carefully-curated sets of games made for you,” according to Lumosity’s website.

Along with the games, Lumosity features mindfulness training such as meditation techniques to help you relax and gain mental clarity.

4. MediSafe

MediSafe is a great app for people with short- and long-term memory loss. Remembering when to take medications, knowing if you’ve already taken them, and realizing when it’s time to re-order prescription drugs can be a challenge for people with dementia.

MediSafe provides alerts so people can manage their prescriptions safely. For example, the app notifies your caregiver if you miss a medication for the day, or if any of your prescription drugs shouldn’t be taken together.

5. Game Show

Game Show was developed by the University of Cambridge, and some studies have shown that it can help with the early stages of dementia. Users with dementia showed a 40 percent increase in memory and thinking test scores. The app is not a cure for dementia, but it can help slow down the progression of memory and thinking loss.

Along with social interaction and other mentally stimulating activities, mental games may help slow memory loss and keep your mind sharp.

6. Happify

Apps for People With Dementia | Medicare Plan Finder

Living with dementia can be stressful. Happify uses science-based games and activities to help encourage positive thinking and reduce stress. The app’s tools and programs aim to improve emotional well-being.

Leading scientists and experts in the fields of positive psychology and cognitive behavioral therapy developed Happify’s techniques after decades of research. According to the app’s website, 86 percent of people who used Happify on a regular basis reported feeling better about their lives in two months.

7. Iridis

Stirling University developed Iridis to help people prepare their homes to make life with dementia easier. The app offers advice on how to improve color contrast, and furniture and lighting tips to help you deal with your symptoms.

For example, many people with dementia experience loss of appetite as a symptom. Using dishes that contrast in color with your food can help you remember to eat. You may have vision problems, too, and the app will suggest what kind of lightbulbs you should use to make things easier to see.

You can use Iridis to evaluate your home and determine what changes you should make. The app provides a detailed report with recommendations so you or your caregiver can make the best choices to support your condition.

8. Timeless

According to Timeless, this app is a “first-of-its-kind, simple, easy-to-use app for Alzheimer’s patients to remember events, stay connected and engaged with friends and family, and to recognize people through artificial intelligence-based facial recognition technology.”

The app is developed to help Alzheimer’s patients improve their quality of life. The app is simple and helps the user remember events and appointments, and stay connected with friends and family.

Timeless makes use of AI technology to help the user remember faces and names. The face recognition helps to slow down memory loss. Many users may find that the app helps improve their confidence because they’re able to associate their loved ones’ names with their faces.

9. Alzheimer Society’s Talking Point Forum

The Alzheimer’s Society’s Talking Point Forum is a free app developed by the Alzheimer’s Society in the UK. It’s an app for people with dementia and Alzheimer’s that provides a discussion forum.

The app acts as a meeting and discussion place for people to read others’ experiences, ask for advice, share their thoughts, and join in conversations about the issues dementia patients face every day.

The main function of the app is to provide users with a sense of community and help them understand that they aren’t alone. The app can act as a digital support group where people who suffer from dementia and Alzheimer’s can talk to others who understand their situation.

10. A Walk Through Dementia

A Walk Through Dementia helps non-sufferers understand what people with dementia and Alzheimer’s experience. The app was created by Alzheimer’s Research UK and VISYON, and offers insight into the condition with a virtual, immersive platform.

It uses a combination of CGI and 360-degree imaging to see what life is like for Alzheimer’s sufferers.

It uses three scenarios to help users get an idea of what their loved one is going through: 1. The experience buying ingredients at the grocery store. 2. Taking the ingredients home. 3. Using the ingredients to make tea for their family.

This app will help your loved ones better relate to you and empathize with your situation.

Dementia Apps and Medicare Health Insurance to Help Make Life Easier

Along with the above apps for people with dementia and Alzheimer’s, a comprehensive health insurance plan can help make your life easier. If you qualify for Medicare or have durable power of attorney for someone who does, we can help you find a policy that will fit your budget and lifestyle.

Our licensed agents at Medicare Plan Finder are dedicated to helping you learn about the plans available in your area. Call 844-431-1832 or contact us here to find out more today.

Prescription Drug Price Trends

About one in four people say they have a tough time affording their prescription drugs. Prescription drug prices have been on the rise since 2017. According to Rueters, drug companies announced price increases for more than 250 medications in 2019.

According to the Centers for Medicare and Medicaid (CMS), prescription drugs already account for 20 percent of Medicare’s spending, and with the prescription drug price trend increasing, that number will only increase in the near future. That may mean that your vital medications will cost you more.

How to Get Prescription Drug Discounts

Rising prices shouldn’t mean that you have to stop taking your needed drugs. Wouldn’t it be great if you could get a discount for your necessary medications? You can with this free discount drug card!

Prescription Drug Discount Card | Medicare Plan Finder

This discount card is not an insurance plan. However, you can use your discount card to receive up to 75 percent off your prescriptions at more than 68,000 pharmacies. Simply download, print and show your card to the pharmacist when you check out to save money on your important medications.

Why Are Prescription Drug Costs Rising Rapidly?

Senior Man With Pill in Hand | Medicare Plan Finder

The prescription drug price trend may be going up due to a lack of competition for pharmaceutical companies, and mergers and acquisitions in the pharmaceutical industry.

Lack of Competition for Pharmaceutical Companies

Many major pharmaceutical companies own patents for their drugs. That means other manufacturers cannot legally create generic equivalents, and the patent holders can charge whatever they want for their products.

Usually, manufacturers will produce generic drugs once a brand name patent expires. Some drugs are expensive to develop even with an expired patent, so that often means the original manufacturer is the only company producing their drug.

Mergers and Acquisitions in the Pharmaceutical Industry

Drug manufacturers make deals to expand their product bases. Unfortunately, when pharmaceutical companies merge, they get a lot of bargaining power. The pharmaceutical companies can demand that pharmacy benefit managers (PBM) – people responsible for contracting with pharmacies and getting drug discounts – set prices higher. Those costs get passed on to the government and ultimately to you.

Sometimes, pharmacy benefit managers merge with health plans, like in the cases of Cigna and Express Scripts and CVS and Aetna. Those mergers may actually be able to HELP you, by lowering costs due to reduced overhead and improved communication.

Medicare Prescription Drug Price Negotiation Act

One reason the prescription drug price trend is rapidly increasing is that CMS cannot legally negotiate drug prices. The Medicare Prescription Drug Price Negotiation Act is a bill that would require Medicare to negotiate prescription prices with pharmaceutical companies. It was first introduced in the House of Representatives in 2017, and re-introduced in 2019.

Other federal and state entities are making efforts to help reduce drug prices. The Food and Drug Administration is working toward approving more generic versions of brand name medicines. Many states have passed laws requiring drug companies to justify price increases.

Medicare Prescription Drug Plans

Prescription Drugs | Medicare Plan Finder

As prices rise, you may want to consider a new form of prescription drug coverage. Original Medicare does not help pay for prescriptions, but you can get prescription drug coverage through Medicare Part D, or through certain Medicare Advantage (Part C or MA) plans.

You can still use your discount drug card along with your insurance plan. When you go to the pharmacy to pick up your prescriptions, the pharmacist can determine your cost with each option.

Medicare Part D

Medicare Part D plans are also called prescription drug plans (PDPs). You can use PDPs to cover your medication costs. Many people who have PDPs also purchase Medicare Supplement (Medigap) plans to help pay for items such as coinsurance and copays.

Even though Medicare Supplements and Medicare Advantage plans sound similar, they are actually very different. Medigap plans “fill in” the gap between what you owe and what Original Medicare covers. MA plans help pay for medical expenses. If you have questions, one of our highly trained, licensed agents will be happy to help. Your agent can help you find the right plan for your budget and lifestyle.

PDPs typically use formularies that divide medications into tiers according to their copays. For example, one plan may feature four tiers with varying expenses. The first tier may only include generic drugs and cost $5 per prescription. Tier two may include preferred brand name medications and cost $15 per prescription.

Medicare Part D Checklist | Medicare Plan Finder

Medicare Advantage Prescription Drug Plans

Medicare Advantage plans are privately owned insurance policies that cover everything Original Medicare covers, but they can offer additional services including vision, hearing, and dental. Certain MA policies called Medicare Advantage Prescription Drug (MAPD) plans offer medication coverage.

Like PDPs, MAPDs use a formulary that lists every covered drug and separates them into tiers. The difference is that MAPD plans come with only one monthly premium for your covered services, and it includes prescription drugs.

Medicare Over-the-Counter Drug Coverage

Many people use over-the-counter (OTC) drugs along with their prescription medications. Like with prescription medications, Original Medicare does not cover OTC drugs. However, certain MA plans help pay for OTC medications. Some plans feature a pre-paid card that allows you to purchase covered items such as bandages and cold medicine.

How We Can Help You With Rising Prescription Drug Prices

Your agent can help you find a plan that not only includes all of your prescriptions, but covers the additional services you need. Call us at 844-431-1832or contact us here to learn more today.

Contact Us | Medicare Plan Finder

Elder Care Legal Advice: What Caregivers Need to Know

While most of caregiving is handling everyday tasks such as bathing and eating, a lot of legal issues surround elder care. Elder law is the body of rules created to protect the elderly. It covers areas such as legal guardianship and protection against elderly abuse and neglect.

You may have to fight for your loved one or for yourself. Many caregivers also take on estate administration and power of attorney issues along with medical care decisions. It can seem daunting, but we’re here to answer your questions and provide support.

Elderly Abuse

Unfortunately, some people take advantage of the elderly in their vulnerable state and they fall victim to abuse at the hands of nurses, strangers, and even family members. Elderly abuse comes in different forms including physical abuse, financial abuse, emotional abuse and neglect. It can be easy to overlook the signs of elderly abuse, but it is important to pay attention to your loved ones to catch these things early on.

Signs of Elderly Abuse

Nursing home staff or other caregivers may seriously mistreat your loved one. Here’s what to look out for:

Signs of injury such as bruises, welts, or scars, especially if they’re on only one side of the body

Pill bottles that have more or less remaining product than they should

Nursing homes refusing to let you see your loved one alone

Money or other items missing from the senior’s home

Malnourishment not resulting from an illness

Lack of grooming or poor hygiene

Untreated bed sores

Dirt, bugs, soiled bedding or other indications of unsanitary living conditions

Leaving the senior out in the elements with unsuitable clothes

Substandard living conditions such as faulty wiring or lack of heat or running water

Huge cash withdrawals from the senior’s bank accounts

Multiple bills for the same medical service or device

Evidence of subpar care when bills are fully paid

Problems with the care facility staff: poor training, poor pay, or understaffing

Leaving the elder behind in public

As a caregiver, you must be an advocate, even if you can’t fix the problem yourself. If the person under your care is abused in any way, seek elder care legal advice from an attorney who focuses on elder law to find the best course of action.

Federal Anti-Abuse Programs

If you don’t know where to look for professional elder care legal advice, start with these federal resources:

The National Center on Elder Abuse (NCEA) is dedicated to preventing elder abuse and raising public awareness. The NCEA website provides information about a variety of important topics such as elder rights and how to report elder abuse.

The National Family Caregiver Support Program (NFCSP) is a fantastic source for locating abuse prevention resources and legal assistance. The NFCSP also provides a wealth of information for caregivers including disease-specific educational materials and contact information for local support groups.

Power of Attorney

Law Library | Medicare Plan Finder

You should start planning for mental incapacity as soon as your loved one is diagnosed with a chronic disease such as Alzheimer’s. You may want to enlist in the help of an elder law attorney who can give you in-depth elder care legal advice. Your lawyer will help you with estate planning and determining who will make financial and medical decisions.

Both power of attorney and legal guardianship are tools that allow caregivers to make important decisions on behalf of the seniors under their care. The difference is that guardianship requires a court decision, while a senior can choose a power of attorney when he or she is of sound mind.

In many cases, the best course of action is for your loved one to appoint a power of attorney early on so that you can step in to make important decisions as soon as you need to.

There are three different types of power of attorney. The differences between each boil down to when legal decision-making power starts and stops:

Conventional power of attorney: Starts when the senior signs the power of attorney document and stops when the senior becomes incapacitated.

Springing power of attorney: Starts when the senior becomes incapacitated.

Durable power of attorney: Starts when the senior signs the document and continues until the end of his or her life.

Caregivers and seniors benefit most from the caregiver having a durable power of attorney to make healthcare decisions.

Medicare and Power of Attorney

Caregiver Discussing Power of Attorney With Senior Woman | Medicare Plan Finder

If the person under your care is 65 or older, is diagnosed with ALS or ESRD, or receives SSDI for at least 25 months, he or she will qualify for Medicare. You’ll need to have legal authority in order to help enroll your loved one in a Medicare plan.

The Medicare beneficiary under your care can decide the scope of your responsibilities as a caregiver. Depending on where you live, a power of attorney may give you an all-encompassing authority to make financial decisions such as selling real estate or making donations to charity, or it can be limited to healthcare decisions.

Medicare has protections in place that limit access to medical information to people other than the beneficiary. It’s useful to have the person under your care fill out a form authorizing Medicare to release medical information to you. You might need to prove that you have durable power of attorney to access the healthcare information.

Guardianship

At some point, many seniors won’t be able to take care of themselves or make important decisions on their own. You can become a legal guardian for the elder by going through these legal proceedings:

File a petition with the court in your state.

Tell the elderly person along with his or her family about the petition for guardianship.

Comply with a court investigation to determine whether guardianship is necessary.

Engage in a hearing during which the judge looks at investigation results and listens to the senior in order to make a decision regarding the petition.

Legal Protection You Have As a Caregiver

The Family Medical Leave Act (FMLA) allows eligible employees up to 12 weeks of unpaid leave to care for immediate family members who have serious illnesses. FMLA requires that you return to the same or equivalent position upon your return, and your employer must continue to provide the same group health insurance during your leave. You don’t have to take the leave all at once.

If your employer refuses to grant qualifying leave, you should show them a printed copy of the law. If that doesn’t work, ask an employment lawyer to draft a letter. If your employer still refuses to grant leave even after the letter, you can sue for FMLA violations.

You can also sue if your employer retaliates and fires you or drastically changes your working conditions. Talk to your employment lawyer or your state’s Department of Labor to find out if your situation warrants a lawsuit.

You are not alone as a caregiver. Organizations such as Caregiver Action Network (CAN) provide a wealth of support to caregivers all over the US. Caregivers will find a community of like-minded people who are having a similar experience. CAN aims to make caregivers’ lives easier by providing resources such as where to find elder care legal advice and education specific to their seniors’ conditions.

How We Help Caregivers

Medicare Plan Finder can help you or a loved one find the right health insurance plan. Our mission is to serve the seniors you care about the most. Having power of attorney can be a lot of work, especially when you have to think about your own family and career. We can guide you through finding a Medicare plan for your loved one if you have power of attorney. Call us at 844-431-1832 or submit this form today.

Contact Us | Medicare Plan Finder

This post was originally published on May 13, 2019, and was updated on June 28, 2019.

6 Tips to Find the Right Dentist That Takes Medicare

Oftentimes, people wait until it’s too late to visit the dentist. Many common oral health problems don’t even have noticeable symptoms right away, but your dentist can catch them.

Regular dental exams and cleanings should be a part of your healthcare routine. If you’re eligible for Medicare, you may want a dentist that takes Medicare insurance to help cover dental costs.

However, even if your dentist takes Medicare, you could be missing out on a huge opportunity for better care. Use these six tips to find a better dentist.

1. Find the Right Dental Insurance, First

Before you select a dentist, make sure that you have dental insurance coverage with a network that allows you to pick your own dentist.

Original Medicare will only provide dental coverage for medically necessary services. That means dentists cannot accept Medicare Part A or Part B for routine dental care. However, some private insurance plans called Medicare Advantage plans can help pay for services that Original Medicare does not, like hearing, vision, and of course, dental.

It may seem difficult to find out what insurance plans dentists take in your area. You may not even know where to start. Our licensed agents are highly trained and can help you locate dentists that take Medicare Advantage plans.

Some people may need coverage for more dental services than Medicare Advantage plans provide. You can purchase separate private dental insurance plans that may provide the additional coverage you need. Talk to your agent about private dental insurance plans.

2. Learn What Other People Say About Local Dentists

Other people are a great resource for learning about dentists in your area. Ask friends and family what they think about their dentists, or ask your doctor for a referral. You can also find information from professional associations such as the American Dental Association (ADA) or the Academy of General Dentistry (AGD).

Even though you can find plenty of reviews on Google, be wary of fake accounts. If a review looks like a machine wrote it or it’s too over-the-top, proceed with caution.

3. Check out the Dentist’s Website

Woman Looking at Dental Websites | Medicare Plan Finder

The ADA has a directory website that allows you to search for dentists in your area by specialty. For example, let’s say you have good oral health, and you want to find a general dentist. The ADA directory will show you all of the local dentists who are ADA members and their contact info.

The dental practice’s website will display much of the information you need such as the insurance plans they accept, operating hours, address and contact information.

Take the office’s location into account, and ask yourself if you can get there easily. Assess whether their business hours fit into your schedule.

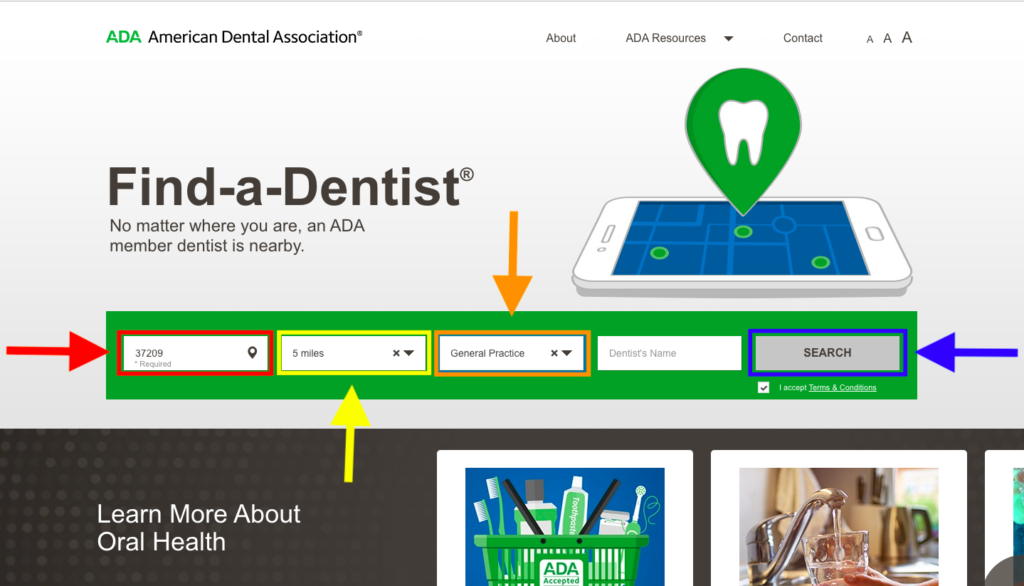

How to Use the ADA’s Local Dentist Finder Tool

Click here to use the ADA’s local dentist finder tool. Enter your zip code in the box beside the red arrow. We used our home office zip code, which is 37209. Then, in the box above the yellow arrow, select how close you want your dentist to be. The next step is to select your dentist’s specialty, which you can do in the box under the orange arrow. Then click “SEARCH” beside the blue arrow.

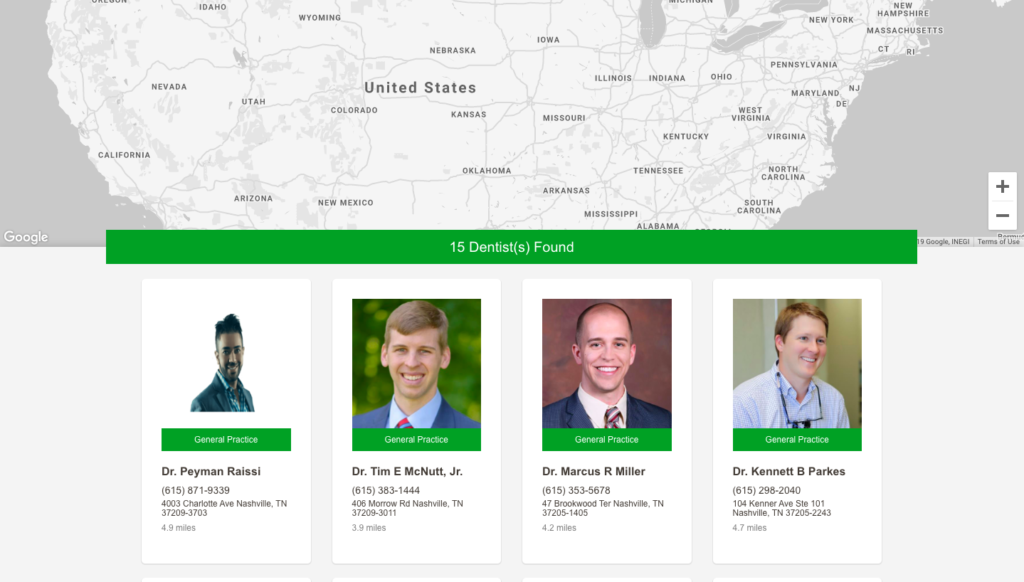

Then you’ll come to your list of local ADA dentists.

4. Make Lists of Offered Services

You have an idea of what services you might need. For example, if you have dental implants, you may need to find a periodontist or an oral surgeon who specializes in gum disease. However, if you’ve only had a couple of cavities and you only need routine cleanings and examinations, a general dentist may be a better fit.

As you browse dental websites, list what services they offer and compare the services with your needs. You may find that only a couple of dentists in your area specialize in your condition, or you may find that you have many options.

5. Visit the Facility

Once you’ve narrowed down a few choices, visit their offices. Look around and ask yourself if the facility is neat and organized. See if dental staff wear protective equipment such as gloves and if they seem to enjoy their jobs. Listen to how the staff talks to patients.

You want to get an idea of what your experience might be like if you make this person your regular dentist. If you like what you see, consider making an appointment.

6. Compare Costs

Dentist and Patient Discussing Treatment Plan | Medicare Plan Finder

Even if you find a dentist who accepts your insurance plan, you may still owe some bills. Make an appointment for a consultation and have the dentist make an itemized list of the services you need and their costs.

If the dentist recommends a long list of costly treatments such as oral surgery, veneers, or crown replacements, you may want to get a second opinion.

We Can Help You Find Dental Coverage

Finding the right dentist can seem overwhelming. Your Medicare Plan Finder agent may be able to help you find the right Medicare Advantage or private dental insurance plan. Call 844-431-1832 or contact us here today.

11 Crucial Tips for Taking Care of Elderly Parents at Home

Taking care of an elderly parent at home may be the most important thing you ever do, but it can be easy to get bogged down with the day-to-day struggles you may encounter.

You can help minimize your physical and financial stress that can come with caring for aging parents with some planning and resources. Follow these 11 tips to set yourself up for caregiving success.

1. Monitor Medications

One vital part of caregiving is making sure your parent receives his or her medications on time. Many pharmacies have apps that allow you to set up automatic refills for qualifying prescriptions, and you can even have prescriptions mailed directly to you.

It’s important to find a health insurance plan that will help pay for all of your parent’s medical needs. Medicare is a fantastic resource for paying medical expenses, but Original Medicare may not cover all of the services your loved one needs, such as prescription drugs.

You may have to look into private insurance policies called Medicare Supplements or Medicare Advantage plans to cover additional services and ensure that your parent’s insurance meets his or her needs.

If you need help paying for your parent’s medications, Medicare Part D or certain Medicare Advantage plans offer prescription drug coverage. There may be many plan options out there for you, and asking a qualified professional for help finding the right one may make the difference in your loved one receiving the right care.

2. Find Assistive Devices to Help Make Life Easier

As your parent ages, he or she may have difficulty performing actions such as bathing, standing up, or walking, and you may consider using assistive devices or Durable Medical Equipment (DME) to help make life easier. Assistive devices for the elderly range in supportive functions from fall prevention and mobility (canes, walkers, wheelchairs) to helping button shirts or clean.

Medicare Part B will help cover DME if your doctor prescribes the devices. You may owe deductibles or coinsurance. Some items such as wheelchair ramps and handrails may not be considered DME, but some Medicare Advantage plans cover those home modifications.

3. Hire Outside Help if Necessary

At some point, your parent may require more help than you can provide. You may have to enlist the help of skilled nurses or other healthcare professionals to perform the required level of care. If you don’t know where to start looking, your parent’s doctor may recommend a home healthcare service, or Medicare has a registry where you can find agencies in your area.

If it’s extremely difficult for your parent to leave the house, Medicare will cover intermittent skilled nursing services, meaning that the skilled professional doesn’t visit your parent every day or for extended periods of time.

Some parents will need long-term care, and Medicare will not cover those services. You can, however, purchase long-term care insurance to help pay for expenses such as a full-time nurse.

4. Make Sure Your Loved one Stays Active

Healthy Seniors Lifting Dumbbells | Medicare Plan Finder

An active lifestyle that includes regular exercise may help prevent chronic diseases. Resistance training combined with cardiovascular exercise can help manage symptoms of osteoporosis, diabetes and chronic hypertension. Go on walks with your parent, go to the pool or look for fitness classes geared toward seniors such as Silver & Fit® or SilverSneakers® in your area. Certain Medicare Advantage plans cover fitness classes.

5. Find Proper Nutrition for Your Loved One

Ensuring that your parent eats properly can be time-consuming. You may be responsible for grocery shopping, meal preparation, and making sure your loved one eats at the right times throughout the day. Not only that, but your parent’s doctor or dietitian may recommend that your parent eats a certain number of calories or that your parent’s diet focuses on lean protein sources, fruits, and vegetables.

You can cut down on the time it takes for meal preparation by preparing meals for a few days in advance and putting them in single-serving containers. Look for recipes with simple cooking methods such as using a slow cooker or one-pan meals.

Some Medicare Advantage plans even cover meal delivery, which would dramatically cut down on the time you spend worrying about your parent’s nutrition.

6. Create a Schedule

Creating a schedule and sticking to it is extremely important when taking care of elderly parents at home. You’ve got a lot to do for yourself and your loved one, and if you don’t establish a routine for house cleaning, running errands, or bathing, then those things may not get done.

Take some time every week and make a list of everything you and your parent need to accomplish. Create a calendar that includes all of the events for the week because seeing doctor’s appointments, meal delivery times, etc. will help you coordinate everything your parent needs and also let you schedule some time for yourself.

7. Take Time to Care for Yourself, Too

Smiling Woman in Meditative Pose | Medicare Plan Finder

It can be easy to forget about self-care when you’re so involved with your loved one, but taking some time for yourself is extremely important.

Find some time to relax. Take bubble baths, meditate, or do anything else that makes you happy. The important thing is that you feel refreshed and recharged when you go back to your parent.

Be active. Exercise is not only beneficial for your physical health, but also your mental health. The vast majority of people who exercise regularly report lower stress levels than sedentary individuals. Consider doing yoga, jogging, cycling or joining the gym where your parent takes fitness classes.

8. Find a Support System

Self-care may look like finding a support group or therapist so you can talk about how you feel. Your job as a caregiver may be overwhelming if you feel like you’re alone. If you can openly talk about what’s going on and get information on how to cope, you can provide better care because you’ll have better emotional health.

Sometimes you may just need a break, but you’re unable to leave your loved one alone.

Ask other family members to step in when you need some time off or it could be time to consider finding respite care services, which allow you to rest. Respite care may mean that your parent stays in a hospital temporarily or goes to adult day care.

Medicare will only cover respite care if it’s part of hospice, but the NFCSP or National Association of Area Agencies on Aging (N4A) can help you find respite services in your area that may be in your budget.

9. Know Your Rights

You have rights as a caregiver. The Family Medical Leave Act (FMLA) allows employees who meet certain requirements to take up to 12 weeks per year off to care for qualifying immediate family members.

If your employer has 50 or more employees, you must be allowed to return to your original position or its equivalent when you return to work.

If your employer fires you or demotes you, or refuses to grant leave, you may have a case against your employer for FMLA violations and workplace discrimination.

Talk to an employment lawyer or to your to the Department of Labor if you think your rights have been violated.

10. Obtain Power of Attorney to Make Important Decisions

Caregiver Helping Parent With Power of Attorney Paperwork | Medicare Plan Finder

In order for Medicare to allow you make decisions for your parent, you must first have the right kind of power of attorney (POA). There are many different types of POA, but a Durable Power of Attorney is the only kind Medicare will accept, and it’s the most beneficial for taking care of elderly parents at home. A Durable Power of Attorney will allow you to make medical decisions for your parent before he or she becomes incapacitated.

11. Find Government Assistance for Caregivers of Elderly Parents

Taking care of elderly parents at home can be a full-time job. You may be able to find government assistance for caregivers of elderly parents and receive payment for your hard work. Medicare will not pay for you to provide caregiver services, however, Medicaid will in some states.

It may feel like you’re all alone, but there are some federal resources that can help ease your stress. The National Family Caregiver Support Program (NFCSP) provides a wealth of resources to caregivers information on where to find support groups, educational materials for specific conditions and contact information for advocacy organizations. You’ll be a better caregiver if you use the government resources available to you.

We Can Help You and Your Loved One Find Coverage for Home Care Services

The right insurance plan can help cover the cost of at-home care services. If you have power of attorney, a highly-trained licensed agent with Medicare Plan Finder may be able to help you find a plan that fits your budget and lifestyle needs. Call 844-431-1832 or contact us here to learn more.

Does Medicare Cover Genetic Testing for Melanoma (MyPath)?

Malignant melanoma is a type of skin cancer that starts in the skin’s pigment-producing cells. About two percent of people will develop melanoma in their lifetime, and 5-10 percent of those cases are hereditary.

Parents with specific gene mutations have about a 50 percent chance of passing those genes to their children. Genetic testing for melanoma can reveal the gene mutations associated with skin cancer and allow you to seek treatment right away.

Medicare Coverage for Genetic Skin Cancer Testing

Doctor Discussing Cancer Testing Results | Medicare Plan Finder

Anyone who is eligible for Medicare has some financial assistance available for their healthcare. Medicare can help pay for expenses such as doctor appointments for diagnosing and treating melanoma. Medicare will cover genetic testing for melanoma if you have certain risk factors.

Melanoma is just one type of skin cancer. The most common types of skin cancer are called carcinomas and they are usually the result of exposure to UV rays. Melanoma can be attributed to certain gene mutations.

Medicare will only cover genetic testing for cancer if it’s medically necessary. Currently, Medicare offers coverage for the Myriad Genetics myPath and the Castle Biosciences DecisionDx tests.

Myriad Genetics myPath

The myPath Melanoma test from Myriad Genetics measures 23 genes and differentiates melanoma from normal cells. The genes in the test include:

PRAME one gene involved in the process where a cell changes from one type to a different type

S100A7, S100A8, S100A9,S100A12 and PI3, a group of genes involved in the cell communication process that regulates cell activities

CCL5, CD38, CXCL10, CXCL9, IRF1, LCP2, PTPRC and SELL, involved in the immune system response to tumors

Measurements of nine housekeeping genes (genes that maintain basic cell function) to use as a baseline in determining normal gene expression

Castle Biosciences DecisionDx

Castle Biosciences offers the DecisionDx-Melanoma test to help doctors determine if a patient has Stage I or Stage II melanoma. The test screens for the following genes:

Does Medicare Cover Genetic Testing for Melanoma | Medicare Plan Finder

Along with genetic risk factors, several other factors may mean you’re more likely to develop melanoma, including:

Fair skin: People with fair skin have a much higher risk of developing melanoma than people with darker skin. Those with red or blonde hair, blue or green eyes, or skin that freckles easily and is susceptible to sunburn are at an increased risk of developing melanoma.

Personal history of melanoma or other skin cancers: If you’ve already had melanoma or another type of skin cancer, you could be at risk for it again.

Having a compromised immune system: Your immune system fights off cancer and other diseases. If your immune system is weak as a result of certain diseases or medical treatments, you’re more likely to develop melanoma.

Age: Melanoma is more likely to occur in older adults than younger adults.

Sex: Men older than 50 have a higher rate of melanoma than women.

Xeroderma pigmentosum: People with xeroderma pigmentosum (XP) have a high risk of developing melanoma. XP is a rare condition that interferes with the skin’s ability to repair DNA damage.

Melanoma Statistics and Facts

Melanoma is becoming more common, and it can often be treated if it’s caught early.

Melanoma rates have been steadily rising for the last 30 years.

The American Cancer Society estimates that there will be approximately 96.5 new melanoma diagnoses and about 7,200 melanoma deaths in 2019.

Melanoma’s five-year survival rate is about 97 percent when the cancer is detected early. If the disease spreads to the lymph nodes, the survival rate declines to 68 percent, and to 15 percent if the cancer reaches other organs.

Treatment for Melanoma

Treatment for melanoma is different depending on the stage of cancer (I-IV), where it is on your body, and your overall health.

Stage 0: These melanomas have not penetrated the top layer of skin yet. A wide excision surgery will remove the melanoma and a small amount of normal skin around it.

Stage I: Wide excision surgery will also remove these melanomas, and also portions of normal skin around them. The amount of normal skin removed depends on how thick the melanoma is, and where it is on the body.

Stage II: Surgery to remove the melanoma and some of the normal skin around it is also the treatment for stage II melanoma. Many doctors will also recommend a lymph node biopsy, because cancer may have spread to the lymph nodes near the melanoma.

Stage III: In stage III melanoma, the cancer has already reached the lymph nodes when it’s first diagnosed. The treatment usually involves removing the melanoma with surgery, and dissecting the lymph nodes around the tumor. After the surgery, doctors will recommend prescription drugs for immunotherapy or targeted therapy for cancers with BRAF gene changes.

Stage IV: These melanomas are often difficult to cure because they have already spread to lymph nodes far from the melanoma. Skin tumors or enlarged lymph nodes can oftentimes be surgically removed or treated with radiation therapy. If the cancer has spread to internal organs, it can be removed depending on how many incidents of cancer there are, where the incidents are, and how likely the cancer is to cause symptoms. Other treatments include immunotherapy drugs and chemotherapy.

Contact Us Today

Medicare can cover specific genetic testing for melanoma and skin cancer treatment if you meet certain criteria. If you need coverage beyond what Original Medicare pays for, private health insurance plans called Medicare Advantage plans or Medicare Supplements may better suit your needs.

A representative with Medicare Plan Finder can help you find the right Medicare plan to fit your budget and lifestyle. Call us at 844-431-1832 or contact us here to learn more today.