Understanding Medicare Part B – Coverage and Costs for 2020

What Is Medicare Part B?

Medicare is a federal government health insurance program for seniors 65 and older and others who meet qualifying conditions.

Medicare consists of four parts, labeled A, B, C, and D. Parts A and B make up the government-funded “Original Medicare” program. Part C refers to “Medicare Advantage” plans, which provide additional medical insurance. Part D refers to separate prescription drug Medicare plans.

Part A covers costs associated with hospitals and other inpatient services. It’s complemented by Part B, which covers outpatient services, preventative care, and durable medical devices.

Some people are automatically enrolled in Parts A and B while others must enroll on their own.

What is the difference between Part A and Part B Medicare?

Part A is often referred to as Medicare “hospital insurance,” while Part B Medicare coverage is often referred to as “medical insurance.” What this means is that while Part A can cover hospital stay charges, Part B can cover your doctor’s appointments and preventative care. If you had Part A only, you would have coverage for hospital care, but not any of your doctor’s appointments, so it’s important to enroll in both.

Medicare Part B Coverage

At this point, you’re probably wondering, “what does Part B of Medicare pay for?”

Medicare Part B covers ambulance services, doctor visits, preventative services, mental health, women’s health services (like mammograms), lab tests and X-rays, some medical equipment, and more. It does NOT cover hospital stays or most prescription drugs. The only time that Part B will cover drugs is if the drug is administered by a medical professional.

Medicare Part B Drugs

Here is a list of drugs covered by Medicare Part B:

Drugs used with durable medical equipment, like nebulizer supplies

Antigens, when prepared and administered by a doctor

Injectable osteoporosis drugs if medically necessary

Erythropoiesis-stimulating agents for those with ESRD or anemia related to other conditions

Oral ESRD drugs

Blood clotting factors for those with hemophilia

Other injectable and infused drugs when given by a medical professional

Preventative Services and the Annual Wellness Visit

Medicare Part B includes 100% coverage for several preventative services.

For example, when you first enroll in Part B, you can make a “Welcome to Medicare” appointment with your doctor. This will be a comprehensive overview conversation with your doctor about your healthcare needs and concerns.

You will also be eligible for an Annual Wellness Visit. This is more in-depth and includes a health risk assessment, a review of your and your family’s medical history, measurements (height, weight, BMI, blood pressure, etc.), mental health screenings, and a general conversation about your daily health concerns.

Also included under Part B at 100% coverage are your preventative vaccines, such as annual flu shots. However, some vaccines that are not considered preventative measures are not included under Part B coverage.

For example, the Shingles vaccine would be covered under Part D coverage instead of Part B.

Preventative services are also covered for:

high blood pressure

high blood sugar

abnormal cholesterol

obesity

glaucoma

depression

cardiovascular disease

HIV

smoking and alcohol cessation

various cancers

Women are covered at 100% for pap smears, pelvic exams, and breast exams every two years. If you are diagnosed as at-risk for gynecological conditions, you may be able to receive screenings every year instead.

Mental Health

Medicare Part A covers inpatient mental health care. Part B covers outpatient mental health services, including:

No-cost yearly depression screenings

Both individual and group psychotherapy (including family counseling)

Psychiatric evaluations and diagnostic tests

Certain prescriptions

Medication management

Limited partial hospitalization

Partial hospitalization refers to psychiatric hospital treatments that don’t require an overnight stay. Items like meals, transportation, and support groups are not included.

You will only receive coverage when you see a doctor or specialist who accepts Medicare. You will be responsible for 20% of most of these services. There may be additional co-payments or coinsurance for partial hospitalization.

IMPORTANT: If you or a loved one is in immediate crisis, call the National Suicide Prevention Lifeline immediately at 1-800-273-8255 (TTY 1-800-799-4889). Help is available 24-7.

Laboratory Tests and X-Rays

When your doctor orders a lab test to help diagnose a condition or as part of your annual checkup, you are covered under Part B. Medically necessary blood tests and other diagnostics sent to a lab are covered.

They include blood work, urine tests, tissue lab work, and some screenings at no cost to you.

Blood for transfusions is handled differently. If you get a transfusion through a blood donation, you may not have to pay anything. Otherwise, you may have to pay 20% of the Medicare-approved amount.

X-rays are also covered but at 80% of the Medicare-approved amount. You are responsible for the other 20%.

Emergency Transportation

Part B can cover emergency transportation if other transportation could put you in danger or you are having a medical emergency and need immediate assistance. It will only cover an ambulance ride to the nearest medical facility that can give you the type of care you need.

You cannot request to visit a hospital that is further away.

Air transportation is covered only if you need to get to a facility quickly and cannot do so by ground transportation (heavy traffic, inaccessible road conditions, etc.)

Transportation is covered at 80% of the Medicare-approved amount, and your Part B deductible will apply.

In some cases, Part B may cover non-emergency ambulance transportation if there is no other safe way for you to get to a hospital or other provider office for medically necessary services.

You will need to schedule your ambulance transportation in advance by reaching out to a non-emergency ambulance transportation company like ACC Medlink and Lifeguard.

The company you select may charge a fee and can contact Medicare to request authorization for coverage.

Durable Medical Equipment

Part B will only cover durable medical equipment.

For an item to be considered durable medical equipment (DME), it must be able to withstand repeated use for at least three years, must be usable at home, and must be used for a medical purpose only. Medicare will cover 80% of the cost.

In some cases, you may be able to choose whether you want to rent or purchase the equipment you need.

Some examples of DME include:

Blood sugar test strips and monitors/glucose control

Canes, crutches, scooters, walkers, and wheelchairs

Check with your doctor or Medicare to see if an item is considered a DME or not.

Long-Term Care

Part B covers some home health care, but only that which is relatively short-term and related to a limited period of recovery due to an illness, injury, or condition. Part B does not cover long-term care, either at home on in a nursing facility, that people may need due to frailty or because they need help with daily activities (bathing, grooming, eating, etc.)

What isn’t covered by Medicare Part B

Medicare Part A and Part B are structured to work together to provide maximum coverage at an affordable cost for most Americans.

This coverage is enhanced by adding optional Part C Medicare Advantage or Medicare Part D drug plan coverage.

In general terms, Part A covers in-hospital expenses, and Part B only covers outpatient expenses, durable medical equipment, and wellness activities.

Medicare does not cover anything not considered medically necessary. That includes elective and cosmetic surgery and several forms of alternative medicine such as homeopathy, acupuncture, and acupressure. Chiropractors are covered on a limited basis.

Other than flu and pneumonia shots, Medicare does not cover vaccinations and immunizations. The exception is if there is a health emergency, and vaccinations are required to stem the risk of infection through a contagious disease.

Part B also only covers drugs you can’t self-administer. Coverage is only provided if you receive medications in a hospital, doctor’s office, or health clinic. This is where Part D coverage can come in handy. All nonprescription drugs and remedies are also not covered under Part B.

General dental work is also not covered, unless it would need to be performed by a physician, meaning the treatment would be considered medical vs. dental

Part B also does not cover vision care, hearing aids, or contact lenses, except those required after cataract surgery. But if your eyes are affected by an illness or injury other than a routine loss of vision, you will be covered for ophthalmological services.

Routine foot care is also not covered unless a foot condition is the result of conditions such as diabetes, cancer, multiple sclerosis, inflammation due to blood clots, chronic kidney disease, malnutrition. Care must be diagnosed as medically necessary.

Except in rare circumstances, medical services outside of the United States and its territories are not covered as well. You will need to enroll in a Medicare Advantage plan for international coverage.

Medicare Part B costs in 2020/2021

Medicare premiums, copayments, and deductibles are adjusted annually according to the Social Security Act. What will Medicare Part B cost 2020 enrollees?

In 2020, the standard monthly premium is rising by about 7% due to increased program costs, up to $144.60. If you already get Social Security or Railroad Retirement benefits, your premium can be deducted from those. Social Security Medicare Part B payments will be automatic for most people.

The standard deductible is $198. After you pay your deductible, you’ll have to pay 20% for most Medicare Part B services, other than preventative and wellness services detailed above.

There is no income limit for Medicare Part B, but if you have a high gross income, you could be required to pay an Income-Related Monthly Adjustment Amount (IRMAA).

Some people may purchase a Part C plan that offers low deductibles and copays. You will pay a Part C premium, but you could wind up with more comprehensive coverage that will significantly augment existing Part A and B coverage and provide Part D prescription drug coverage as well.

Who qualifies for free Medicare B?

Unlike Medicare Part A, the amount of time you’ve worked does not affect your Part B premiums. Most people will have to pay a premium for Medicare Part B. To qualify for free Part B, you’ll have to qualify for one of the following programs:

The Specified Low-Income Medicare Beneficiary Program (SLMB) offers premium assistance for Part B. If you are eligible for an SLMB, you also are automatically eligible for an Extra Help program to assist in Part D prescription drug coverage.

Individual monthly income limit = $1,269

Married couple monthly income limit = $1,711

Individual resource limit = $7,730

Married couple resource limit = $11,600

The Qualified Individual Program (QI) also helps pay Part B premiums. To apply, which you must do every year, contact your state Medicaid program. Enrollments are on a first-come, first-served basis.

Individual monthly income limit = $1,426

Married couple monthly income limit = $1,923

Individual resource limit = $7,730

Married couple resource limit = $11,600

Eligibility for Medicare Part B

Medicare Part B eligibility is based on age, citizenship, retirement benefits, and qualifying illnesses. You are eligible for Medicare Part B if:

You are 65 or older and a U.S. citizen or permanent legal resident.

You are younger than 65 and have qualifying disabilities or suffer from End-Stage Renal Disease or Amyotrophic Lateral Sclerosis (ALS, Lou Gehrig’s disease).

You are eligible to receive, or you’re currently receiving Social Security or Railroad Retirement Board benefits.

If you are aging into the Medicare program, you should enroll in Part B any time between three months before your 65th birthday to three months after.

One question we hear a lot is, “I already have Part A, can I add Medicare Part B anytime?” Unfortunately, it’s not that simple. If you choose to forgo Medicare Part B when you first became eligible, you could face a late enrollment penalty fee later. Additionally, if you don’t enroll when you first become eligible, you’ll have to wait for the open enrollment period from January 1 through March 31 to enroll.

If you get Social Security or Railroad Retirement Board benefits for at least four months before your 65th birthday, you’ll automatically be enrolled in Part A and Part B coverage. Coverage starts the first day of the month you turn 65.

When you’re under 65, you have a disability, and you have been getting SSDI benefits for at least 24 months, you are automatically enrolled in Part A and Part B. If you suffer from Amyotrophic Lateral Sclerosis (ALS or Lou Gehrig’s disease), you are automatically enrolled in Part A and Part B the month your disability benefits begin.

If you have been diagnosed with End-Stage Renal Disease (ESRD), you can enroll in Part A and Part B. To get full benefits that cover dialysis and kidney transplant benefits, you’ll need to be covered by both.

Check with Medicare.gov, because there are several stipulations regarding coverage for ESRD.

You can enroll in Part B during your Initial Enrollment Period (IEP), the General Enrollment Period (GEP), or during Special Enrollment Periods (SEP) if you qualify.

You can sign up for Part B benefits the following ways:

Call Social Security at 1-800-772-1213 (TTY: 1-800-325-0778).

If you worked for a railroad, call the Railroad Retirement Board at 1-877-772-5772.

Medicare Part B phone number: For questions about Medicare Part B billing, call 1-800-833-4455.

What happens if you don’t sign up for Medicare Part B?

While you are technically not required to sign up for Medicare Part B, you may face a late enrollment penalty fee if you wait too long to enroll. This will come in the form of a premium increase of as much as 10%.

Can I delay Medicare Part B coverage?

You can delay signing up for Part B coverage, but if you enroll at a later date, you may have to pay an enrollment penalty. This penalty will be in force for the entire time you have Part B coverage.

When you delay Part B coverage, it also means you can’t sign up for a Part C Medicare Advantage plan. One of the requirements for Part C is that you must currently be enrolled in Parts A and B.

Additionally, if you miss your initial enrollment period for enrolling in Part B, you’ll have to wait until the enrollment period from January 1 through March 31 to enroll.

Can I decline Medicare Part B coverage?

Is it mandatory to have Medicare Part B? No. But make sure you do your homework first and take into consideration your long-term health needs.

Although you have to pay a premium in many cases for Part B coverage, it still makes sense to enroll for a vast majority of people.

Is Medicare Better Than Individual Plans?

Is Medicare Better Than Individual Plans?

One survey about Medicare satisfaction vs. private insurance satisfaction found that people with Medicare were happier with their health plans than people with individual plans. Will you find the same to be true?

Types of Plans

As you turn 65 or otherwise become eligible for Medicare, you probably have a lot of questions. What’s going to change? Will I lose or gain new benefits? The good news is that signing up for Medicare does not necessarily mean giving up your plan flexibility or your favorite doctors. There are plenty of Medicare options available, and we’ll explain why it’s worth it to go ahead and get signed up as soon as you can.

Employer Coverage

You can purchase health insurance through your employer, as long as it meets the coverage limits set by the federal government. If you’re retiring but aren’t eligible for Medicare yet, you can use COBRA to hold you over. COBRA allows you to continue receiving your employer coverage for a short period of time (but your employer likely won’t help you pay for it except for in some unique cases).

You can also technically have Medicare and employer coverage at the same time, if you become eligible for Medicare while you are still employed. That might make sense for some people and not others.

Private Coverage

You can purchase insurance from an exchange like Healthcare.gov, directly from your state, or directly from a health insurance company. Generally, purchasing private insurance is more expensive than employer coverage, and much more expensive than Medicare and Medicaid.

TRICARE/VA Coverage

Veterans and veteran’s families may be eligible for free or low-cost healthcare through the Department of Veteran’s Affairs (VA). You or your spouse must have served for at least 24 continuous months or teh full length of time that you were called to serve for. You can also qualify if you were honorably discharged. To get TRICARE, you must already be enrolled in Medicare Part A and Medicare Part B. Click here to read more about coverage for veterans.

Medicaid

Medicaid is a federal health program. Each state has slightly different rules and each state has its own funding. The program can cover any person of any age with low income (according to the Federal Poverty Level and with some adjustments in each state). Most Medicaid beneficiaries will have either no or very small premiums. If you have a low monthly income AND are over 65, you may qualify for both Medicaid and Medicare! In that case, you can get what is called a “Dual-Eligible Special Needs Plan,” which is low-cost and tailored to your needs.

Medicare

Original Medicare is a federally funded health program that can cover any adult over the age of 65 as well as some adults with disabilities, such as end-stage renal disease.

Most people with Medicare will start with parts A and B. Part A provides hospital coverage, and Medicare Part B provides medical coverage. Anyone who wants more coverage can opt to enroll in either a Medicare Advantage plan or a Medicare Supplement (also called Medigap) plan. Medicare Advantage is sometimes referred to as “Part C” because you have to have Part A and Part B first to enroll in it, and it can cover a lot of services that parts A and B do not.

Unless you enroll in a Medicare Advantage plan that includes prescription drug coverage, you’ll want to enroll in a separate drug plan. These plans are referred to as “Medicare Part D,” because they are completely separate from the other “parts.” Part D plans only cover prescription costs.

Some people may qualify for no or low-cost Medicare coverage, but others will have to pay premiums. Most people will not have to pay nearly as much for Medicare as they would with an individual or private health plan.

You may think that individual plans provide more coverage due to the higher premiums, but that is not always the case. All Medicare plans include preventative services. Plus, you can choose to enroll in Medicare Advantage, which is like a private plan for Medicare. With Medicare Advantage, you can roll all your benefits – medical, dental, vision, prescription drugs, and even fitness – into one convenient plan.

How is Medicare different from other health insurance?

Medicare is vastly different from other health insurance options for a lot of reasons, ranging from the way you pay for your coverage to when you can enroll.

For starters, the Medicare enrollment period is different from the ACA enrollment periods and your employer’s enrollment periods. The Medicare Annual Enrollment Period runs from October 15 through December 7, but be sure to not confuse it with the ACA Open Enrollment Period, which runs from November 1 through December 15 of each year.

Another thing that is different is that some people can have their Medicare Part A payments automatically deducted from their Social Security check.

Employer Health Insurance vs. Medicare

It’s hard to even compare Medicare vs. employer health plans because the only thing they have in common is that they provide health insurance. If you’re turning 65 or otherwise preparing to make the switch from your employer plan to Medicare, you should know the pros and cons of each option.

For starters, Original Medicare is the same for everybody. Technically, there are not separate plans to choose from within the government Medicare program. Once you’ve enrolled in Original Medicare, you can decide to add coverage through a private Medicare Advantage or Medicare Supplement plan. Some people may see this as a great thing because you can enroll right away without stressing about all your options. Others don’t like it, because one plan clearly cannot work for everybody. However, that’s what the private plans are for (and many of them are incredibly cheap compared to employer plans – some even have $0 premiums).

The advantage of private health insurance for Medicare (Medicare Advantage or Medicare Supplement) is that you can pick and choose which benefits are most important to you so that you aren’t paying for coverage that you don’t need. Plus, some people will qualify for Medicare Special Needs Plans which are specifically designed for people with special financial or medical needs and are usually relatively low-cost plans. Private Medicare plans can closely resemble individual marketplace plans or employer plans.

The disadvantages of private health insurance for Medicare-eligible people are that they sometimes have limited doctor networks and that some areas might have a limited number of plans to choose from. Typically, people who live in rural areas may have fewer plan options when it comes to private Medicare coverage.

Medicare vs. Medicaid

Both Medicare and Medicaid are government programs that are regulated by CMS (Centers for Medicare and Medicaid Services). They both provide health insurance for medically necessary services.

The main difference between Medicare and Medicaid is who qualifies. It is possible to qualify for both programs, but Medicaid qualifications are based on income while Medicare qualifications are based on age and disability. Another difference is that while the Medicare qualification rules are federal, Medicaid qualification rules can change slightly by state.

Medicare Versus Spouse Insurance

A lot of people who are newly qualified for Medicare wonder if it might be better to stay on their spouse’s insurance plan. The fact is, it depends on how good your spouse’s insurance is. However, if you do qualify for Medicare, Part A (the part that covers hospital costs) has a $0 premium for anyone who has worked and paid Medicare taxes for at least ten years. If you haven’t worked that long but your spouse has, you might still qualify. If that’s the case, there’s no reason not to go ahead and enroll in Medicare Part A as soon as you become eligible.

Additionally, if you wait too long to seek out further Medicare coverage, your costs may go up. You can be charged a penalty of up to 10% of your premium if you don’t enroll in Medicare Part B when you first become eligible. Plus, Medicare Supplement plans can charge more or deny coverage based on preexisting conditions if you wait too long to enroll. So if you think you might want to enroll in a Medicare Supplement plan, don’t wait too long to start looking.

Medicare vs Other Health Insurance: The Benefits

If you are eligible for Medicare coverage but considering alternative health insurance, you should start by learning what Medicare does and does not cover. Medicare Part A and Part B are the same for all who enroll. They cover preventative healthcare, like your annual wellness visits and flu shots at 100%.

Part A also covers 60 consecutive hospital days at 100%. After the 60th day, you’ll start to owe co-payments. Part B covers mental health, lab tests and X-rays, emergency transportation, and medical equipment.

Medicare A and B do not include prescription drug coverage, dental, vision, hearing, podiatry, or any service that is not deemed medically necessary either for treatment or prevention. For additional health coverage, millions of Medicare beneficiaries enroll in Medicare Advantage.

Since Medicare Advantage plans are owned by private companies, they can add in benefits like dental, vision, hearing, etc. – any of those extra benefits that you might be accustomed to from having private health insurance. Some Medicare Advantage plans also cover prescriptions. If you want prescription coverage but don’t care about all of the extra benefits, you can enroll in a stand-alone prescription drug plan instead. However, you cannot have both a Medicare Advantage plan and a Medicare prescription drug plan at the same time, so choose wisely.

Medicare vs Other Health Insurance: The Costs

The good news about Medicare is that as long as you or your spouse have worked and paid Medicare taxes for a certain number of years, your Part A Medicare costs will be low.

If you or your spouse has worked and paid Medicare taxes for at least 40 quarters, you’ll owe $0 in Part A premiums.

If you or your spouse has worked and paid Medicare taxes for 30-39 quarters, you’ll owe $252/month in 2020 in Part A premiums.

If you or your spouse has worked and paid Medicare taxes for less than 30 quarters, you’ll owe $458/month in 2020 in Part A premiums.

Part B premiums are standard for all Medicare beneficiaries. It can change each year, but the Part B monthly premium in 2020 is $144.60, and the deductible is $198. Most services that Part B covers are covered at 80%, so you may owe 20% coinsurance or doctor co-payments.

If you choose to enroll in a prescription drug plan, a Medicare Advantage plan, or a Medicare Supplement plan, you may face an additional premium.

Medicare vs. Private Insurance Costs

If you’re choosing between enrolling in Medicare Part B versus private insurance, remember that delaying your Part B enrollment can leave you with up to a 10% increase in your premium when you do decide to enroll.

If you decide to add on private Medicare insurance through a Medicare Advantage or Medigap plan, remember that you’ll still have to pay your Medicare Part A and B monthly premiums (unless you qualify for a savings program such as QMB). You cannot enroll in MEdicare Advantage without enrolling in Medicare parts A and B first.

Medicare Advantage and Medicare Supplement plans are completely separate and therefore come with separate bills. You’ll owe a premium (which in some cases can be $0), and you’ll likely have a deductible as well as co-payments for certain services.

Many private health insurance plans also have out-of-pocket maximums, which means that if you have a lot of health care costs, you can reach a point where you stop having to pay out-of-pocket for services. Those out-of-pocket expenses can really start to add up even with Medicare if you’re someone who needs a lot of medical care!

Why is Medicare cheaper than private insurance?

A lot of new Medicare beneficiaries do find that their Medicare costs are cheaper than what they were paying before they qualified. The biggest reason for that is the way Medicare is funded. While you or your spouse were working hard for all those years, you were paying Medicare taxes. Your low premiums today are because of all that hard work! Plus, the Medicare office does not incur nearly the same amount of administrative costs that many healthcare companies do.

Is it better to have Medicare or private insurance?

Is Medicare a good insurance option? Is private health insurance better? It depends on who you ask. This is a great question to ask an insurance agent who knows what sort of medical expenses you have and what your budget is.

The main difference you have to remember when you’re wondering if private insurance or Medicare is better is that private insurance gives you more plan options. To get a private Medicare Advantage plan, you’ll have to enroll in Medicare A and B, first. Then, you can choose if you want to personalize your coverage and add benefits by enrolling in additional medical insurance.

If you’re stuck between Medicare and keeping your employer plan, remember that you could face penalties if you don’t enroll in Medicare when you first become eligible – and nothing says you can’t keep both!

Is Medicare or private insurance better for people with dependents?

If you have dependents, Medicare isn’t going to help you. But that doesn’t mean you shouldn’t enroll. Medicare only provides individual coverage – there are no family plans or spouse Medicare plans. However, your Medicare Part A might be free. If that’s the case, you might want to consider enrolling in Medicare for yourself first, and then taking a look at options for your dependents.

If you have access to an employer plan, do the math to figure out if it may be more cost-effective for you to have your group vs. individual Medicare Advantage coverage. In some cases, it might even make sense for you to keep both. If your Medicare Advantage premium is low enough, you can keep that for yourself but also hang onto your group coverage for as long as you can to support your family. An insurance agent can help you figure out what’s best for you.

Can I drop my employer health insurance and go on Medicare?

If you become eligible for Medicare while still receiving employer health insurance, you can and should still enroll in Medicare to avoid penalty fees.

First, find out if you’re currently in one of the Medicare enrollment periods. Medicare open enrollment is different from your employer’s open enrollment period.

If you just became eligible, you’ll have a few months for your “Initial Enrollment Period.” If you’re aging into the program, this period begins three months before your 65 birthday and ends three months after. If you’ve already missed that period, don’t panic – you can enroll for the first time from January 1 through March 31 of each year.

Once you’re enrolled, the “Annual Enrollment Period,” is when you can add or make changes to your Medicare coverage. It runs from October 15 through December 7 of each year. This period is not for enrolling in Medicare for the first time – it’s only for adding or making changes to your private Medicare coverage.

According to Medicare.gov, some people will be automatically enrolled in Medicare Part A upon becoming eligible. If you are not automatically enrolled, you can apply for Medicare on the Social Security website.

How Medicare Works with Other Insurance

Millions of Medicare beneficiaries opt to enroll in Medicare Advantage or Medicare Supplements on top of their Medicare coverage. In these cases, the private insurance companies act as the “secondary payers.” Health benefits that Medicare does not cover will be automatically billed to the private company, but anything else will go to Medicare first. If you have both employer insurance and Medicare, Medicare might actually be the secondary payer. Check with your employer or your employer’s health insurance plan to be sure.

Both Medicare and private insurance coverage will have limitations – so having both is a great way to keep yourself and your families financially covered in case of a medical emergency.

How Medicare Plan Finder Can Help You

We specialize in Medicare and serving the underserved senior and Medicare-eligible population. Do you or a loved one need help selecting a Medicare plan that truly helps? Set up a free appointment with one of our licensed agents in your area to get bias-free assistance. Call us to set it up at 1-844-431-1832.

7 Important Things You Never Knew About Medicare

What is Medicare? Most people are familiar with short answer: Medicare is a federal health insurance program that covers people over the age of 65, people with certain disabilities, or those who suffer from either ESRD (end-stage renal disease) or ALS (Lou Gehrig’s Disease).

While this is probably the easiest way to explain Medicare, most people don’t know how complicated it can be once you dive below the surface. Here we’ve broken down the 7 most important facts about Medicare that you may have never heard before!

1. There are multiple parts of Medicare

Perhaps the biggest misconception about Medicare is that it’s one gigantic program. In truth, what we refer to as Medicare actually has four distinct components, or “parts.” You might hear some different names used but usually these parts will be designated as A, B, C, or D.

The Original Medicare program consists of Part A and Part B. Part A primarily covers inpatient hospital care, while Part B handles outpatient services like doctor visits. These two components of Original Medicare represent the basic coverage that is available to you when you turn 65.

Part C, often called Medicare Advantage plans, are offered by private health insurance companies. These allow recipients of parts A and B to also receive benefits like dental, vision, and prescription drug coverage depending on the plan they choose.

Medicare Advantage | Medicare Plan Finder

Part D, sometimes called a prescription drug plan (PDP), offers prescription drug coverage to beneficiaries enrolled in Medicare. These are offered by private insurance companies as an addition to the Original Medicare benefits, as Original Medicare does not include any drug coverage.

To see these different Medicare plans explained in even more detail, check out our more in-depth blog here on finding the best types of Medicare plans for you in 2020!

2. You can’t enroll whenever you want

Unfortunately, Medicare is not a program you can just enroll in at any time. It’s true that you are eligible for Medicare when you turn 65, but unless you qualify for automatic enrollment, you will need to sign up during one of the five designated enrollment periods.

The Initial Enrollment Period (IEP) is usually your primary opportunity for Medicare enrollment. If you are aging into the program, this IEP begins three months before your 65th birthday and extends to three months after, giving you seven months in total to enroll.

There is actually a second IEP, sometimes called IEP2, available for those who are eligible for Medicare before they turn 65, such as those with disabilities. This period also lasts seven months and gives these beneficiaries an opportunity to make changes to their plan.

The General Enrollment Period (GEP) is offered for first-time Medicare enrollees who did not join during their IEP. This period occurs every year from January 1 to March 31. Coverage applied for during this period begins on July 1st.

The AEP, or Annual Enrollment Period, starts every October 15 and runs until December 7. This period provides an opportunity for those already enrolled in Medicare to make changes to their coverage, such as adding a Part D plan or converting your Original Medicare to a Medicare Advantage plan.

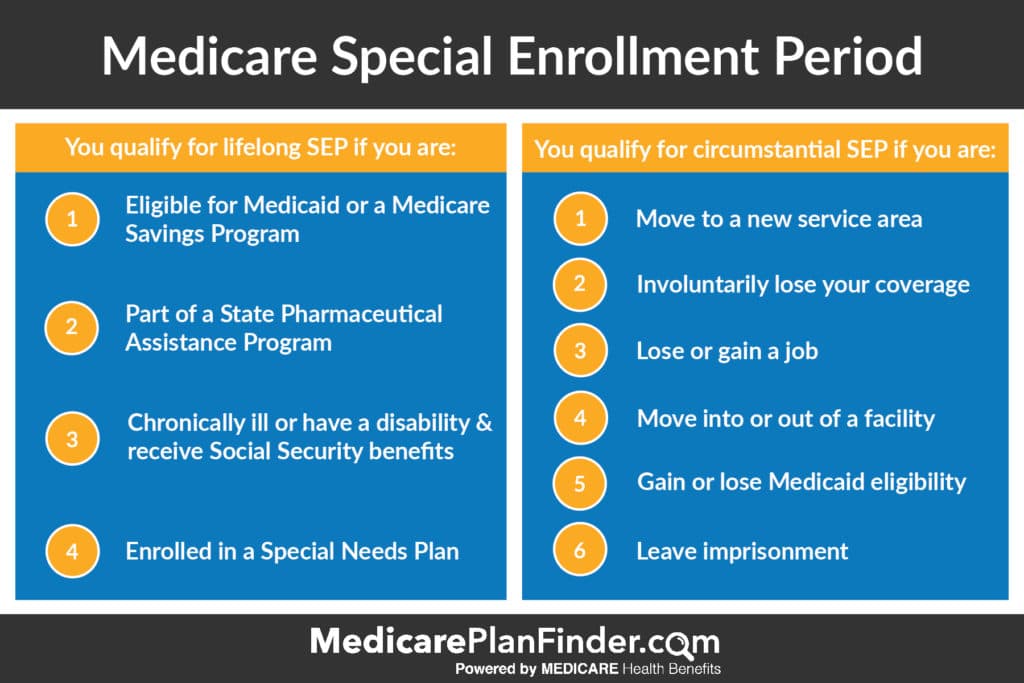

Special Enrollment Periods (SEPs) allow Medicare beneficiaries to make changes to their coverage outside of AEP. During these periods, people who are enrolled in a Special Needs Plan or who have recently lost a job can add to or switch their coverage. Check out the handy graphic below to see if you qualify for one of these SEPs.

Special Enrollment Period | Medicare Plan Finder

In 2019, a new enrollment period was introduced, called the Open Enrollment Period, or OEP. This period lasts from January 1 to March 30, and lets those who enrolled in Medicare Advantage during AEP make changes in their coverage without having to wait for the next AEP.

3. You may have to pay if you delay

If you do miss your IEP, you may have to pay penalties when you finally do enroll. The amount you will pay and the duration you will have to pay depends on which part of Medicare you enroll in and how long you waited.

The Part A penalty is incurred if you do not qualify for free, automatic enrollment and you fail to sign up for it when you are eligible. This penalty will be added to your premium to the tune of 10%, which you will have to pay for twice the number of years that you neglected to sign up.

If you enroll late in Part B, your premium will go up by about 10% for every year you were eligible but didn’t sign up. You will then have to pay this increased premium for the entire time you have Medicare Part B. You may also have to pay a penalty if you do not enroll in a Part D plan within the first three months that your Parts A & B are active. However, some of these penalties may be avoided if you qualify for a Special Enrollment Period.

4. Original Medicare only covers 80%

Once you are finally enrolled, you might wonder: “How much does Medicare cover?” The unfortunate truth is that it will not fully cover your medical expenses. Parts A & B will only cover up to 80% of the cost of Medicare-covered services, leaving you to pay the remaining 20% coinsurance.

This might not be too much trouble for routine doctor visits, but in the case of a medical emergency or hospital stay, the amount you pay out-of-pocket can skyrocket quickly. To cover that last 20%, consider purchasing a Medicare Supplement plan to add on to your Original Medicare coverage.

5. Original Medicare doesn’t cover dental, hearing, or vision

Many people might not realize that Medicare covers very little in the way of dental and hearing expenses, and virtually nothing when it comes to vision. Part A will sometimes pay for specific dental services if you have to get them while you are staying in a hospital, but will not pay for cleanings, fillings, dentures etc.

Medicare will sometimes cover diagnostic hearing exams if your physician orders it as part of their treatment, but will not cover hearing aids under any circumstances. For vision coverage, your options with Original Medicare are even more limited, as it will not pay for eye exams, glasses, or contact lenses.

There are some options that can provide vision, hearing, and dental coverage for seniors. A DVH (or Dental, Vision, Hearing) plan can be purchased to add to your Original Medicare benefits, or you might look to a Medicare Advantage policy to consolidate all of that coverage into one plan.

If you think Part C might be the best coverage option for you, click here or give us a call at 844-431-1832 to have a licensed agent help you compare Medicare Advantage plans!

6. Original Medicare will not cover you abroad

Aside from a few very specific circumstances, Medicare Parts A and B will not cover your health care while you are traveling outside the United States. Medicare Part D plans are also invalid once you are more than 6 hours away from a U.S. port.

But there are some Medicare coverage options available for foreign travel, primarily in the form of Medicare Supplement (Medigap) plans.

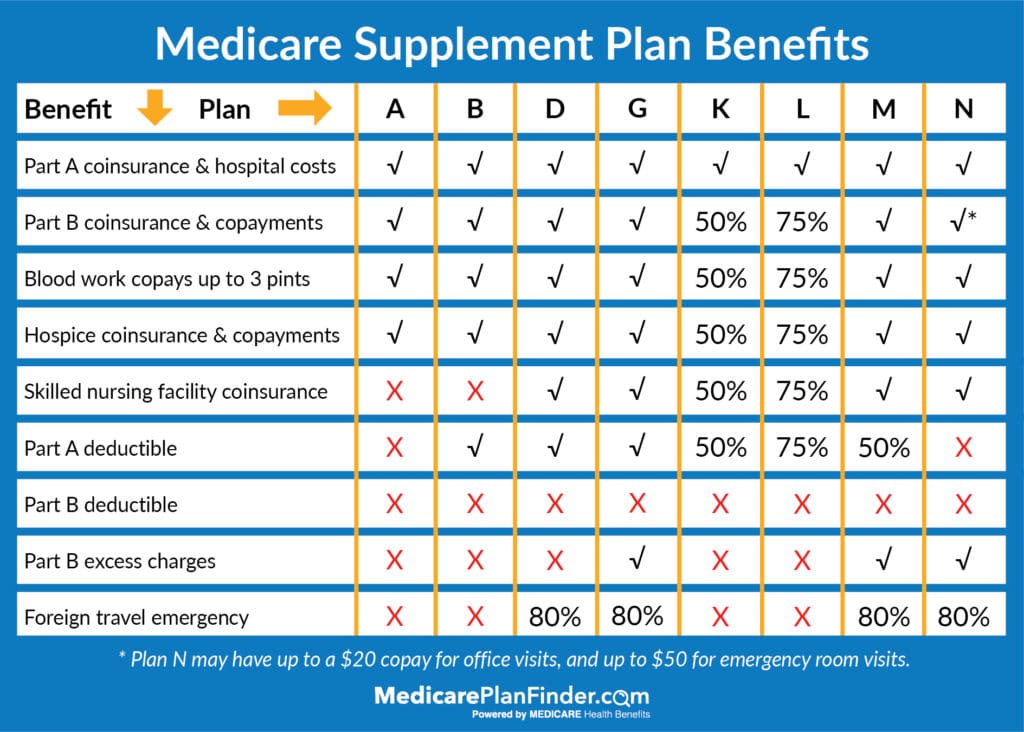

7. Supplement plans have the same coverage, different cost

Medicare Supplement, or Medigap, insurance can be used to cover the out-of-pocket costs you may have to pay with Parts A and B. Insurance carriers offer many different types of Medigap plans, often sorted alphabetically, but they all must follow the same government regulations.

This means that Plan F from one carrier must provide the same benefits as Plan F from another carrier. Below is a quick breakdown of all the benefits covered by the different Medigap plan types.

2020 Medicare Supplement Comparison Chart

Once you have found a Medigap plan type that meets your needs, you must consider the price. Insurance carriers must cover what is mandated by the government guidelines, but may charge very different rates for that coverage.

To find the best price, reach out to one of our licensed agents here or at 844-431-1832 to have them run a personalized quote, or use our Medicare Plan Finder Tool to compare all the plans offered in your state and county!

What is Medicare Part B Buy Back/Give Back?

Are Medicare Buy Back plans too good to be true?

No!

Can they really put money back into your social security check?

Yes, it’s offered through SOME Medicare Advantage plans but not all.

Here is how it works.

Some Medicare Advantage plans out there that can “buy back” your monthly Part B premiums, ultimately putting money back into your pocket. You’ve likely seen this on TV, but unfortunately it’s misleading as this specific benefit is narrowly used by a few plans across the country.

These plans are effectively paying you instead of the other way around! Let me explain.

Medicare Part B Premiums in 2022

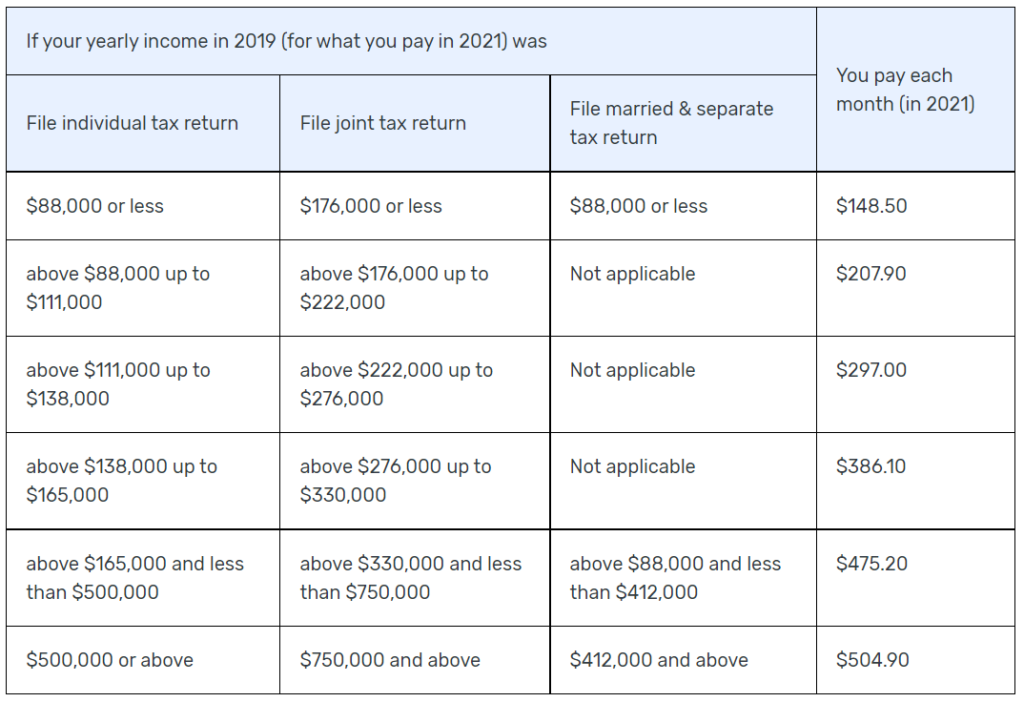

In 2022, the standard Medicare Part B premium will be $148.50. Your premium may be a bit higher if you have a higher income. Below is a snap shot directly from Centers for Medicare and Medicaid about the current Part B premium scale.

The reason you have to keep paying this premium is because Medicare Part B is a paid program, unlike Medicare Part A which you earned during your working years by paying social security taxes. By default, everyone has to pay for Medicare Part B unless they get some kind of financial assistance.

While Medicare Part B is a part of original Medicare, Medicare Advantage plans are privately owned and offer additional benefits beyond original Medicare. In particular, Part B buy back is an additional benefit offered by some plans. This is sometimes confusing to many people, so bear with me.

To have Medicare Advantage, you must be enrolled in original Medicare Parts A and Parts B. In order to be enrolled in original Medicare, you must have worked 40 quarters (or 10 years) paying into social security to earn Part A, and then pay a monthly premium for Part B. To stay enrolled, you have to continue paying your premiums!

You can’t get a Medicare Advantage plan without having original Medicare.

What are Medicare Advantage Part B Buy Back Plans?

Medicare Advantage plans are additions to your existing Medicare coverage. They can vary greatly in coverage amounts and premium prices. Some Medicare Advantage plans can come with a $0 premium or a low premium in addition to a Part B buy back (or give back, as some plans call it).

If you pay your Part B premium automatically out of your Social Security check, this could feel like a bonus added to your monthly checks! You’ll start seeing a bit more coming in, which is nice, assuming the plan you choose has the buy back option.

Premium Give Back Plan? What’s the Catch?

You’re probably skeptical about the idea of an insurance company wanting to give YOU money.

However, there’s not really a catch. According to Quality Health Plans of New York, Medicare Advantage plans “may choose to use some of the funding it receives” to “reduce its members Medicare Part B premium.”

So, what these plans are doing is providing you an incentive to sign up for their plans.

Even if they give you some of that money back for your Part B premiums, they still get paid from your copayments, deductibles, etc.

As you’re looking into available Medicare Advantage plans that offer Part B buy back benefits in your area, be sure to consider what you might be giving up.

Remember, all plans are different, but it is possible that a plan with a Part B buy back option will have higher copayments and deductibles – which may not matter to you if you don’t spend a lot of time in the doctor’s office! The devil is in the details.

I guess you could say the only true “catch” to these plans is that you have to stay enrolled in Medicare parts A and B – but that’s true of any Medicare Advantage plan. You’ll have to continue paying your A and B premiums, even if you do get some of that money back.

Additionally, it may be a few months after you sign up for your premium give back plan before you receive your first Part B reimbursement.

How do I Get a Part B Buy Back (Give Back) Plan?

Great question! As you can imagine, these plans might be harder to find than more standard Medicare Advantage plans, and there may or may not be one available in your area.

Unfortunately, CMS (Centers for Medicare and Medicaid Services) does have certain rules in place that forbid us from sharing the plan details with you publically. However, we have licensed agents across the nation who can meet with you either in person or by phone to help you choose a plan.

If you’re interested, call us at 800-691-1832. Let us know that you’re interested in Part B buy back plans, and we’ll do all we can to help! You can also leave us a message here, and we’ll get back to you.